When You’re Broke and the Bills Don’t Care

If you are wondering what to do when you have no money, start by slowing down, protecting the essentials, and dealing with one problem at a time.

Your rent is around the corner. Your bank app looks like a bad joke. Your inbox is full of “FINAL NOTICE” emails, and your fridge sounds suspiciously empty.

If that’s where you are right now, let’s start with one thing:

You are not a failure. You are a person in a crisis.

And in a crisis, you don’t need the perfect financial plan. You need a clear head, a short list, and one good move after another.

This YesConnected guide is here for that.

It’s written for people in the United States and uses US‑based resources (like 211 and SNAP), but the logic applies anywhere: protect your essentials, calm the chaos, then build a path out.

Knowing what to do when you have no money becomes easier once you separate urgent needs from bills that can wait.

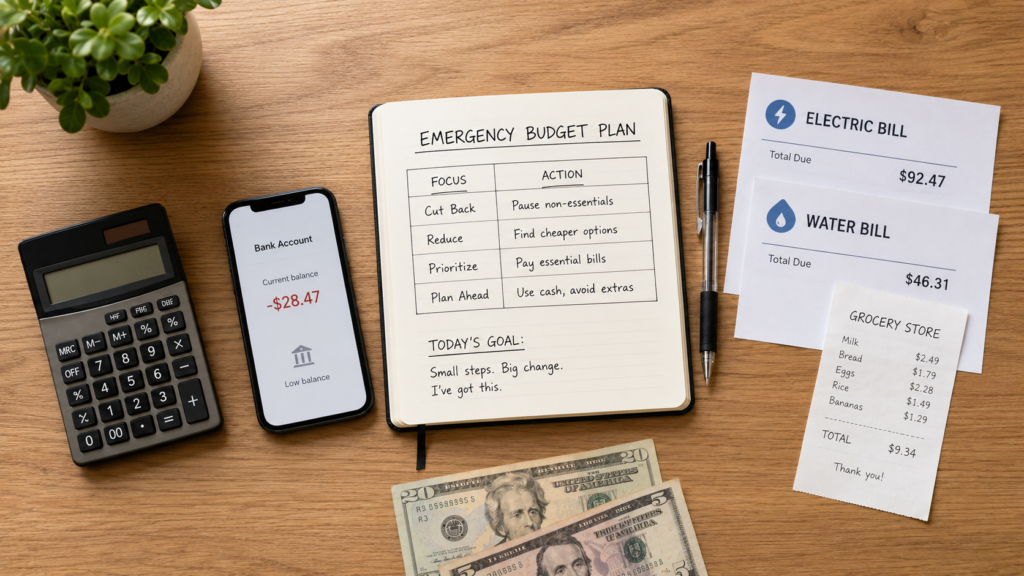

Step 1 – What to Do When You Have No Money: Start With the Numbers

Before you send a single dollar, hit pause.

Give yourself 15 minutes where you are not allowed to pay anything.

Why? Because panic has terrible financial instincts. It pays the creditor who yells the loudest and quietly ignores the bill that can actually get your power cut or your landlord in court.

Take those 15 minutes and do this:

Open your banking app and note:

- Money in checking

- Money in savings

- Any cash you have in hand

Write down:

- Income you expect over the next 7 days

- All bills due in the next 30 days

- Any automatic payments that will hit your account

- What you need for food, medication, housing, and transportation

- What realistically happens if each bill is unpaid

- No guilt. No replay of past mistakes. No “if only I hadn’t bought…”

- You’re not here to judge yourself

- You’re here to draw a map in the dark

If it helps, use a simple table like this:

| Bill / Expense | Due Date | Amount | If Unpaid (realistic) | Priority |

|---|---|---|---|---|

| Rent | In 3 days | $900 | Late fees, possible eviction process | High |

| Electricity | In 6 days | $120 | Service disconnection | High |

| Groceries | This week | $80 | No food at home | High |

| Credit card | Next week | $45 | Late fee, credit score impact | Medium |

| Streaming service | Next week | $15 | Service stops | Low |

Is it pretty? No. Is it useful? Absolutely.

Before you pay anyone, you need this snapshot.

Step 2 – Pay for Survival, Not for Applause

A collector who calls five times a day sounds urgent. Your landlord who sends one quiet email does not.

But urgency and importance are not the same thing.

For each bill, ask yourself one simple question:

“If I delay this, what is the worst realistic consequence?”

Not the worst thing your anxiety can imagine. The worst thing that can actually happen in the next weeks.

For most people, the first priorities look like this:

- Safe housing (rent, mortgage)

- Food

- Essential medication

- Electricity, heating/cooling, and water

- Transportation needed to keep your job or find work

- Insurance that protects your health, home, or car

- Court‑ordered or legally required obligations

Then, after these:

- Other debts, in order of their real impact

- Subscriptions, memberships, and nice‑to‑have services

If you have $40 left, sending $20 to a credit card might feel “responsible”. Using that $40 to get to work all week might actually be the responsible choice.

It’s the difference between looking good on paper and keeping your life functional.

In a crisis, choose functional.

Step 3 – Make the Awkward Calls While Options Still Exist

Most people wait too long to talk.

They leave emails unanswered. They let the shutoff notice sit on the table. They don’t pick up when an unknown number rings.

Not because they don’t care. Because they’re exhausted, ashamed, or out of emotional battery.

But here’s the rule:

Silence is expensive.

Conversation is uncomfortable, but cheaper.

Call before the due date if you can. You do not owe anyone your life story. You just need a clear sentence.

Use this script:

“I’m experiencing temporary financial hardship and I cannot make the full payment by the due date. What payment plans, extensions, hardship programs, reduced‑payment options, or fee waivers are available?”

Then stop talking. Let them answer.

Ask directly about:

A new due date or short extension.

A temporary hardship plan.

A smaller payment for a few months.

Waived or reduced late fees.

Interest‑free installments.

Protection from utility shutoff.

Any “financial hardship” or “low‑income” assistance.

And a key rule: never promise money you’re not sure you’ll have.

“I can pay everything next Friday” sounds hopeful. It becomes a problem when Friday arrives and your account looks the same.

A modest promise you can keep beats a big promise you break.

After every call, write down:

- Date and time

- Who you spoke with

- Exactly what they offered

The new deadline.

Any reference or confirmation number.

If they agree to something, ask for it in writing (email, text, portal message). Verbal kindness is good. Written confirmation is better.

Step 4 – Find Real Help, Not “Secret Methods”

When you’re desperate, the internet fills up with noise:

“Erase all your debt in days.” “Hidden government programs only gurus know.”

“Make thousands from your phone if you buy this course.”

You do not need a guru. You need real support.

In the United States, you can dial 211 to be connected to local help for:

Rent and housing assistance.

Utility bills.

Food.

Medical needs.

Transportation.

Childcare.

Emergency shelter.

Community services.

You may also qualify for programs like:

SNAP – food assistance.

WIC – for eligible pregnant women, new mothers, infants, and young children.

LIHEAP – help with heating and cooling costs.

Lifeline – discounted phone or internet service.

Unemployment benefits – if you’ve lost income.

Temporary cash assistance and support through local community action agencies, churches, and nonprofits.

Use official government sites, known charities, or established nonprofits. If someone wants you to pay to learn about a “secret benefit”, close the tab.

Genuine assistance doesn’t hide behind a paywall and a promise.

Step 5 – Protect Food Before Low‑Priority Bills

Read this twice if you need to:

Using a food bank is not a moral failure. It is you protecting your household.

Food assistance is designed for exactly this moment: when cash is tight and rent, medication, or utilities are competing with groceries.

Every dollar of food you don’t need to buy this week is a dollar that can keep the lights on or the landlord patient.

Look for:

- Food banks and pantries

- Community kitchens

- Religious organizations offering meals

- Local charities

- School meal programs

- SNAP or WIC eligibility

- Community grocery distributions

- Referrals through 211

- Cancelling a streaming service is mildly annoying

- Skipping dinner is dangerous

Step 6 – Build a 7‑Day Crisis Budget (Not a Life Plan)

You do not need a 12‑month spreadsheet with color‑coded tabs and inspirational quotes.

Right now, you need a seven‑day survival budget.

Step one: pause or cancel everything nonessential that you can safely live without for a week:

- Streaming subscriptions

- App and game subscriptions

- Gym memberships

- Takeout and delivery

- Impulse online purchases

- Automatic transfers that might push you into overdraft

Step two: list what you actually need this week.

- Example:

- Essential Need 7‑Day Amount

- Groceries $60

- Transportation $30

- Medication $20

- Emergency buffer $10

- That’s not a Whole New You™

- It’s a pressure‑control system: one week where every dollar has a job

- Be very cautious about canceling anything that:

- Keeps you insured

- Keeps you housed

- Keeps you legally compliant

- Keeps you able to work

- Saving $40 today is not helpful if it creates a $400 crisis next month

If your account is dangerously low, call your bank and ask:

Whether any pending nonessential payments can be stopped.

Whether recent overdraft or other fees can be waived due to hardship.

There is no guarantee, but asking early often gives you more room to maneuver.

Step 7 – Find Cash Without Buying a Fantasy

You do not need:

A “passive income blueprint”.

A luxury‑lifestyle coach.

A course from someone posing with a rented sports car.

You need boring, legal, practical money.

Small amounts of extra income can make the difference between “everything collapses” and “we get through this month”.

Consider:

- Selling unused electronics, furniture, tools, or clothes

- Asking for extra shifts at work

- Taking temporary or event‑based jobs

- Offering cleaning, moving, organizing, yard work, or basic repair services

- Babysitting, tutoring, pet‑sitting, or dog walking

- Completing small freelance tasks (writing, design, admin)

- Returning unused purchases within their return window

- Collecting money someone already owes you

- Asking whether your employer offers earned‑wage access — and reading the fees carefully

- Before accepting any payday loan, cash advance, or “instant money” offer, write down:

The amount you will actually receive.

The total amount you must repay.

All fees.

The repayment date.

The annual percentage rate (APR), if shown.

What happens if you’re late.

Whether you’ll still have enough for food, rent, and utilities after paying it back.

If repaying it creates another emergency next month, it may not be solving the real problem.

Step 8 – Spot Scams Before They Spot You

Scammers are very good at one thing: sounding like exactly what you want to hear when you’re scared.

Be extremely cautious if someone:

- Guarantees debt forgiveness

- Promises a loan “no matter” your credit

- Demands upfront payment to “unlock” help

- Pressures you to act right now

- Wants payment by gift card, cryptocurrency, or wire transfer

- Contacts you out of the blue with “exclusive relief”

- Guarantees a specific credit score increase

- Wants your banking details before clearly explaining the service

- Tells you to stop talking to your current creditors

- Claims access to hidden government money

- As a rule:

The more desperate the promise sounds, the more carefully you should examine it.

Never give financial information to an unexpected caller. Don’t click links in text messages claiming your benefits, stimulus, or loan are waiting — go to the official website yourself.

Slow is safer.

Step 9 – Deal With Specific Bills, One by One

Rent or Mortgage

If your housing payment is at risk, do not disappear.

Contact your landlord or mortgage servicer as early as possible.

Be honest, brief, and specific.

Offer a realistic plan, not a vague “soon”.

Example:

“I can pay $500 this Friday and the remaining $300 on the 15th. Would you be willing to confirm that arrangement in writing?”

Also look for:

- Rental assistance programs in your city or state

- Community action agencies

- 211 referrals to emergency housing help

- Legal aid or tenant‑support organizations

If you receive a formal eviction notice, treat it as a legal document, not a warning shot. Deadlines matter, and rules vary by state. Get local advice.

Utilities (Electricity, Gas, Water, Internet)

Take shutoff notices very seriously.

When you call, ask about:

- Payment arrangements

- Low‑income or hardship assistance

- Seasonal protections (heat, cold weather)

- Medical protections if someone in the home is vulnerable

- Emergency grants or charity programs

- Support through LIHEAP or similar

- Ask this clear question:

“Please walk me through every hardship, emergency, low‑income, and payment‑assistance option available on my account.”

Then write everything down.

Medical Bills

The first number you see is not always the final number you owe.

Request:

- An itemized bill

- Clarification of anything you don’t understand

A payment plan.

Financial hardship discounts.

Charity care or assistance, if available.

A review for possible billing errors.

A lower “self‑pay” price if you’re uninsured.

If insurance is involved, check whether a claim was denied or processed incorrectly. Ask who handles financial assistance or disputes and speak to them directly.

Credit Cards and Personal Loans

If you cannot make a payment, call before you miss it.

Ask about hardship programs.

Request a temporarily lower interest rate.

Discuss reduced payments or different due dates.

Ask for fee waivers or short payment pauses.

Avoid taking one expensive loan just to make a minimum payment on another. Moving debt around without a plan is like rearranging chairs on a sinking boat.

Step 10 – Your 7‑Day Financial Reset

You’re not trying to fix your whole financial life in a week. You’re trying to make it safer and clearer.

Day 1 – Face the Numbers

List your money, expected income, bills, due dates, auto‑payments, and essentials.

Day 2 – Protect the Foundations

Put housing, food, medication, utilities, transportation, insurance, and legal obligations at the top of your list.

Day 3 – Make the Calls

Contact landlords, utility companies, lenders, and service providers. Ask about hardship plans, extensions, lower payments, and fee waivers.

Day 4 – Find Assistance

Call 211. Check government and nonprofit resources for food, rent, utilities, and medical support.

Day 5 – Stop the Leaks

Pause subscriptions. Review auto‑payments. Make sure every remaining dollar has a purpose.

Day 6 – Bring In Money

Sell items, pick up extra work, offer services, return purchases, or complete short paid tasks.

Day 7 – Look 30 Days Ahead

Estimate your income, essential costs, new agreements, and the gap that remains. You don’t need perfection. You need awareness.

At the end of those seven days, every bill may still not be paid.

But:

You will know what’s truly urgent.

You will have spoken to key people.

You will have applied for help you qualify for.

You will have stopped part of the chaos.

That is not failure.

That is progress.

Official Resources (United States)

Use official sites to learn more, check eligibility, or apply (to be added as links in WordPress):

211 – Local help for housing, food, utilities, and more.

SNAP – Supplemental Nutrition Assistance Program.

WIC – Special Supplemental Nutrition Program for Women, Infants, and Children.

LIHEAP – Low Income Home Energy Assistance Program.

Lifeline – Federal program for discounted phone/internet service.

FTC – Federal Trade Commission (scams, debt‑relief warnings).

CFPB – Consumer Financial Protection Bureau (tools for managing and prioritizing bills).

Frequently Asked Questions

What should I do first when I have no money?

If you are trying to understand what to do when you have no money, begin by listing your cash, income, bills, and immediate needs.

Stop all payments for a moment and write down what you have, what’s coming in, what’s due, and what happens if each bill goes unpaid. Then focus on protecting housing, food, essential medication, utilities, and the transportation you need to keep earning income.

Which bills should I pay first?

Prioritize the bills that protect your safety, housing, health, income, and legal position. For most people, that means rent or mortgage, food, medication, electricity, water, transportation, insurance, and court‑ordered obligations.

Where can I get help paying bills?

In the US, dialing 211 can connect you with local resources for food, rent, utilities, transportation, and other emergency needs. Government agencies, local charities, food banks, and community action organizations may also provide assistance.

How can I make emergency money legally?

Sell unused items, ask for extra hours at work, take temporary jobs, offer local services (cleaning, moving, yard work), return eligible purchases, complete small freelance tasks, or collect money someone already owes you. Be cautious of any “opportunity” that requires a large upfront payment or promises instant riches.